Key data & trends

- According to EY‑Parthenon, UK-listed companies issued 62 profit warnings in Q1 2025. (EY)

- In Q2 2025, the number rose to 59 warnings, marking a ~20% increase year-on-year (from 49 in Q2 2024). (EY)

- For the first half of 2025, companies in the FTSE Construction & Materials sector issued 8 warnings (four times the number in H1 of the previous year) and overall the number of warnings issued in H1 was 121. (EY)

- For Q3 2025 there were 64 warnings (reported in the media) and notable that 20% of warnings in that quarter cited weaker consumer confidence as a cause. (The Times)

- While Q1 saw a slight drop year-on-year, the proportion of listed firms issuing warnings in the past 12 months remained elevated (~18%) in Q1. (EY)

Primary drivers behind the warnings

From the data and commentary, the major reasons companies cited include:

- Contract and order cancellations or delays – in Q1, 40% of warnings cited this reason (highest in 25 years of EY analysis). (EY)

- Policy change and geopolitical uncertainty – in Q2, ~46% of warnings cited this, up sharply from ~4% a year earlier. (EY)

- Tariff-related impacts, supply chain disruption, cost pressures – in Q2, one in three warnings (34%) cited tariff-related impacts. (EY)

- Weaker consumer confidence – in Q3, ~19% cited this; for retail companies the proportion was higher (~56%). (Business Money)

- Sectoral stress – for example, within construction and materials there was a sharp increase in warnings; sectors such as software, industrial support services and retail also rank highly. (EY)

Sector & company case-studies

Construction & Materials

- The sector issued eight warnings in H1 2025 — the most since the pandemic period. (EY)

- In Q1 alone, construction firms issued five warnings — equal to the total for all of 2024 in that sector. (EY)

- Underlying issues: weak demand, cost inflation (labour/materials), delayed projects or cancellations, policy/regulatory uncertainty (e.g., building regulation changes, sustainability requirements).

Software & Computer Services / Industrial Support Services

- In Q1 2025, the two sectors with highest warning volumes: Software & Computer Services (10 warnings) and Industrial Support Services (9). (EY)

- These sectors appear vulnerable to order/contract delays, supply chain challenges and technology investment pullbacks.

Retail & Consumer-facing

- Consumer sentiment weakening is translating into warnings — in Q3, for retail companies 56% of warnings referenced weaker consumer confidence. (Business Money)

- Example: B&M, discount retailer, issued a profit downgrade in October 2025 due to an accounting error and weakening performance. (Reuters)

Commentary & implications

- Even though Q1 2025 saw a modest drop in number of warnings vs the previous year, the quality and significance of the warnings remain high: high proportion citing significant structural drivers (policy/geopolitics, contract delays) and elevated share-price falls (average on day of warning up to ~19% in April) reported by EY. (Accountancy Today)

- The elevated rate of warnings (around 18% of firms over 12 months) is described by EY as “a level typically associated with a period of economic shock”. (EY)

- The shift in drivers (e.g., almost half of warnings citing policy/geopolitical uncertainty in Q2) suggests that firms’ challenges are less about short-term cyclical factors and more about structural uncertainty (trade policy, tariff regimes, global order) which may have longer-lasting effects.

- For investors: warnings are a signal of elevated risk among UK-listed companies; sectors with high warning rates may offer less stable earnings and greater downside risk.

- For companies: maintaining resilience — via flexible cost structures, diversified contract pipelines, scenario-planning for policy/trade shifts — is critical. As one EY partner said: “companies must focus on staying nimble by planning for a range of different scenarios and … continuing to build operational and financial resilience.” (EY)

- For the UK economy: the fact that so many warnings cite structural issues rather than purely cyclical ones is concerning — it raises questions about how much growth and corporate performance will be affected if consumer demand, trade regimes, costs don’t improve.

Summary

In summary:

- 2025 is proving to be a challenging year for UK-listed companies, with a high number of profit warnings (especially early mid-year) across multiple sectors.

- The issues they cite go beyond temporary headwinds: contract cancellations/delays, policy/trade uncertainty, tariffs, consumer weak-spots are recurring themes.

- Some sectors (construction, software, industrial services, retail) are particularly exposed.

- The elevated warning rate signals elevated corporate risk in the UK equity market; companies and investors alike are facing a tougher environment.

- Here are case studies and commentary on the surge of profit-warnings issued by UK-listed companies in 2025.

Case Studies

1. B&M Retail

- B&M announced it had made an accounting error of about £7 million relating to overseas freight costs which were wrongly omitted from cost of goods sold. (The Guardian)

- As a result the company cut its profit forecast for the year ending March 2026 to between £470–520 million, down from a previous range of £510–560 million. (Reuters)

- Its shares plunged (up to ~16% at opening) following the announcement. (Reuters)

- Significance: This case illustrates how cost-control / accounting issues combine with broader warning-drivers (rising costs, consumer weakness) to trigger a profit warning. For investors it shows how even discount retailers are becoming vulnerable to increased freight/cost burdens and internal control issues.

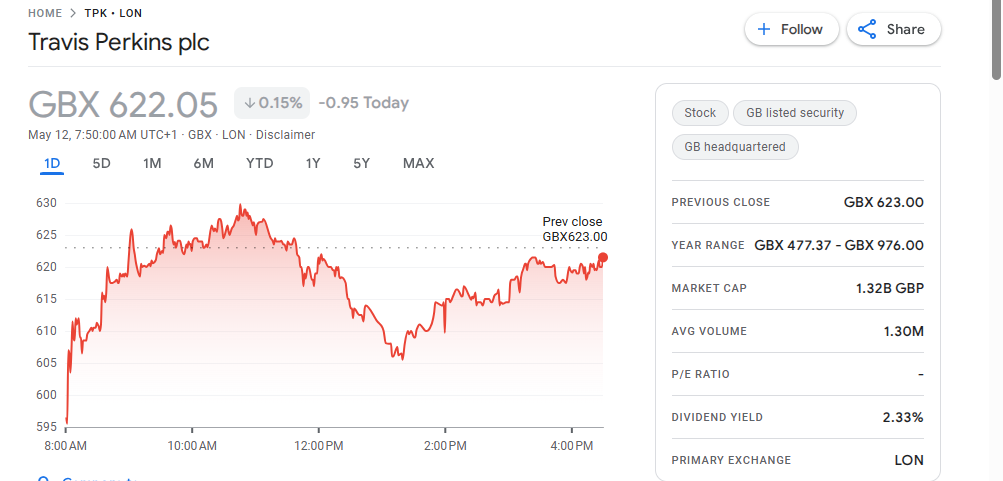

2. Travis Perkins plc

- The building-materials supplier warned that its 2025 adjusted operating profit (excluding property profits) would be broadly flat compared with the prior year (~£141 million), well below analyst expectations. (Reuters)

- Shares fell to a ~15-year low, as the weak UK housing/repair market, high borrowing costs, and subdued demand continue to weigh on the business. (Reuters)

- Significance: A “structural” profit warning rather than purely a one-off: demand weakness in construction, high interest rates, cost pressures all feed in. It underscores why the construction/materials sector is showing elevated warnings. (EY)

3. Sector-wide: Construction & Materials

- According to data from EY‑Parthenon, UK-listed companies in the Construction & Materials sector issued 8 profit warnings in the first half of 2025 — four times the number in the same period in 2024. (EY)

- Overall in H1 2025 there were 121 profit warnings from UK-listed companies. (EY)

- Key drivers in this sector included contract/order cancellations or delays (40 % in Q2), tariff-related impacts (34 %), and policy/geopolitical uncertainty (46 %). (EY)

- Significance: This shows a sector-specific surge of warnings tied to broader macro pressures (costs, policy, trade) rather than isolated company issues. Construction/materials thus becomes a “canary in the coal mine”.

Commentary & Key Themes

- High baseline of warnings: In Q1 2025, UK-listed companies issued 62 profit warnings (down ~11% year-on-year) but the 12-month proportion of firms issuing a warning remained at ~18%. (EY)

- Widening drivers: While contract/order cancellations or delays topped causes in Q1 (40%) (EY), by Q2 the elevated drivers became policy change/geopolitical uncertainty (46% of warnings) and tariff-related impacts (34%) (EY). By Q3, weaker consumer-confidence featured in ~19% of warnings (and ~56% in retail firms) (Business Money)

- Sector concentration: Sectors most exposed include Software & Computer Services, Industrial Support Services, Construction & Materials, and Retail. (EY)

- Implications for investors & companies:

- Elevated warning-rates = elevated risk for earnings surprises.

- Companies must be resilient: diversified contract pipelines, flexible cost bases, scenario planning for policy/trade shifts.

- For investors: higher volatility, caution around sectors with multiple warnings, need to price in risk of further downgrades.

- Macro backdrop: The warnings reflect more than cyclical headwinds; they reflect structural uncertainty (trade, regulation, cost inflation, consumer behaviour) which may persist.

Summary

While 2025 has not (yet) seen an absolute record number of warnings (some quarters down slightly), the intensity, range of drivers, and sector-specific surges make this a particularly challenging environment. The case studies above illustrate how internal company issues (accounting error at B&M) and broader sector weakness (construction/materials) are feeding into the warning statistics.