What is Sterling 20?

- The UK Treasury, working with the City of London Corporation, has launched a new investor-led partnership of 20 of Britain’s largest pension providers/insurers called “Sterling 20”. (Reuters)

- The aim: to channel more pension savings and long-term institutional capital into UK infrastructure, high growth sectors (for example AI, fintech), regional regeneration, housing and other productive assets — thereby supporting the UK economy’s growth and boosting returns for pension savers. (Reuters)

- It builds on earlier voluntary agreements (for example the Mansion House Accord) which set targets for pension funds to invest in UK private markets. (The Guardian)

Key commitments & structure

Here are the headline features:

- The partnership includes leading pension funds/insurers such as Legal & General (L&G), Aviva, M&G, Universities Superannuation Scheme (USS) and others. (Reuters)

- Legal & General has announced a £2 billion commitment by 2030 to invest in “impact investments” across the UK (housing, infrastructure, regeneration) as part of its role in Sterling 20. (Legal & General Group)

- Some funds (e.g., Nest Corporation) are committing additional private market capital, including UK-focused allocations (for example ~£100 million) via money-managers (e.g., Schroders). (Reuters)

- The announcement emphasises regional investment: e.g., boosting affordable housing, broadband in rural areas, urban regeneration, infrastructure outside London. (Express & Star)

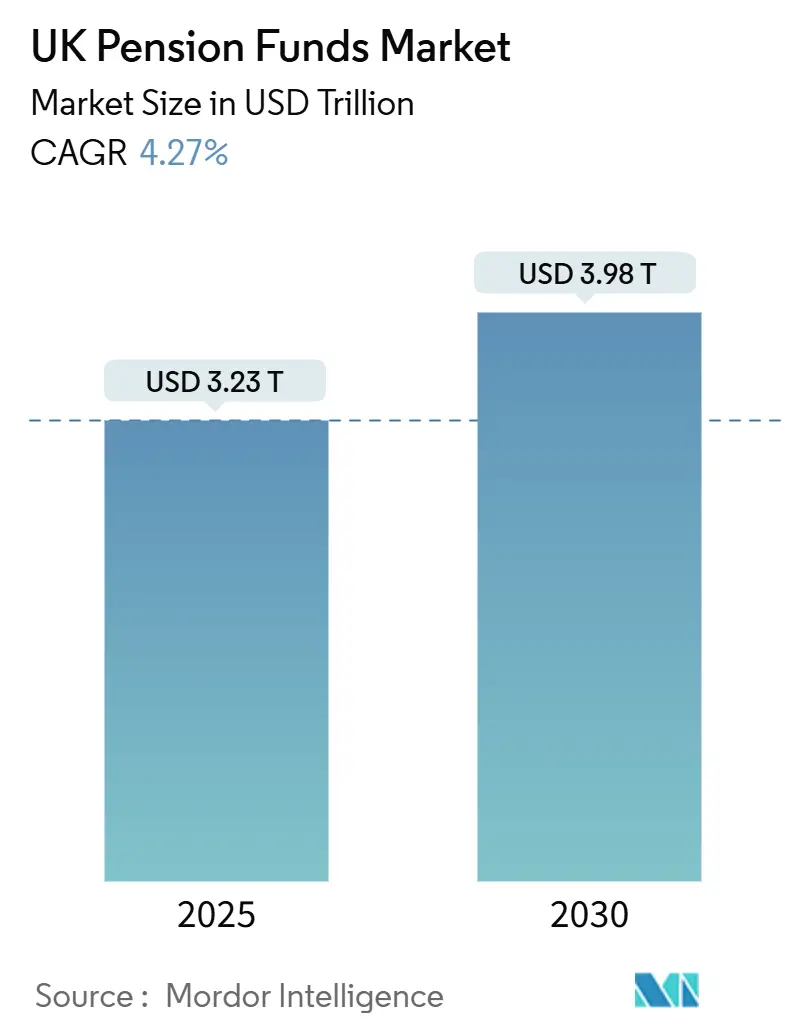

- The total assets under management (AUM) of the participating institutions is enormous — collectively around £3 trillion of assets that could potentially be mobilised. (IFA Magazine)

Why now & what’s driving it

- The UK government is pressing for private investment into infrastructure and growth assets, to boost economic growth, regional balance, jobs, housing supply, and to catch up with countries like Canada and Australia whose pension funds invest more in unlisted assets. (Reuters)

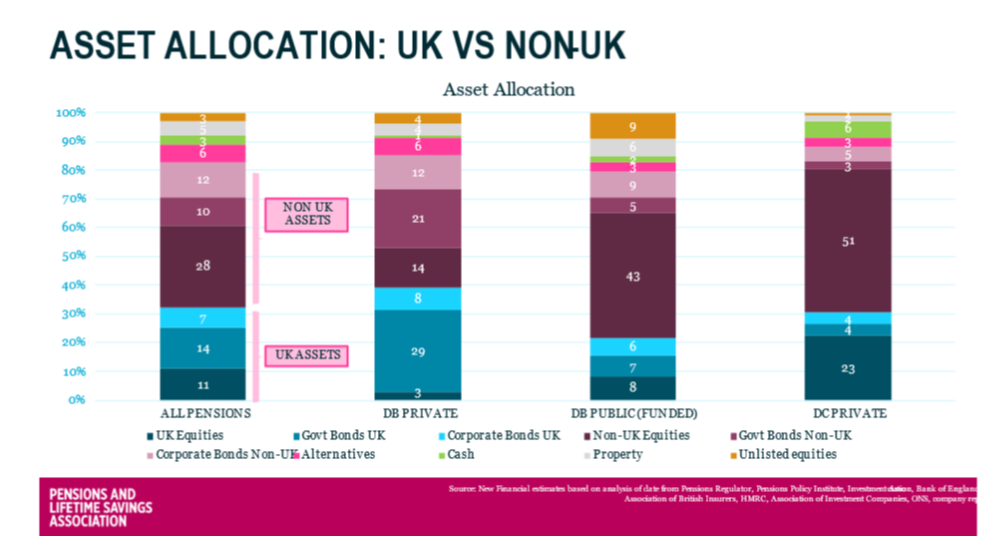

- Pension funds in the UK have historically invested less in private markets/unlisted assets compared to peers abroad, and there is a view that unlocking more of this capital could serve both savers and the national economy. (The Guardian)

- The earlier Mansion House Accord committed major pension providers to invest a certain portion (e.g., 10% of default DC funds) in private markets, with at least half of that in UK assets. Sterling 20 is a next step to operationalise that ambition. (The Guardian)

What this means in practice

- The first wave of commitments shows how this might be deployed: L&G’s £2 billion impact commitment is expected to support ~10,000 new social & affordable homes, create ~24,000 jobs nationwide. (Legal & General Group)

- Some of the targeted asset types: affordable housing, broadband infrastructure in rural areas, scale-up financing for growth businesses, urban regeneration, infrastructure. (Express & Star)

- The initiative will be formally launched at the government’s Regional Investment Summit in Birmingham, linking pension funds, regional authorities and the UK Government. (Reuters)

Benefits & opportunities

- For pension savers: potential for higher returns, better diversification, access to private/infrastructure assets that may provide long-term cash flows and inflation hedges.

- For regional economies: mobilising large capital pools can accelerate housing supply, infrastructure (including broadband), regeneration of under-invested areas, creation of jobs.

- For the UK economy: helps channel billions of pounds of domestic capital into productive use domestically, reducing reliance on overseas investment, strengthening growth.

- For institutional investors: aligning with national/regional priorities may unlock partnerships with government, co-funding, favourable deal flow, scale advantages.

Risks, challenges & caveats

- Asset availability: One key risk is that suitable “shovel-ready” projects might be in short supply, or that the pipeline of investable assets that meet the scale, return profile, and risk/return expectations is constrained. Indeed, commentators have pointed to this. (Reuters)

- Fiduciary duties: Pension fund trustees must act in the best interests of savers. Channeling large amounts into specific domestic/regeneration projects may raise questions about liquidity, risk, return, and alignment with fiduciary duty. Some providers may feel tension between national-growth objectives and saver returns.

- Implementation & coordination: Mobilising £3 trillion of capital across 20 large institutions, aligning on pipeline, governance, regional coordination, deal structuring, risk sharing — this is complex.

- Risk of symbolism vs substance: Some market participants and commentators have warned that unless tangible deals are executed promptly, the initiative could be viewed as more “signalling” than real mobilisation of capital. (Financial Times)

- Market conditions & returns: Infrastructure, real-estate and some private market segments can be illiquid, require long holding periods, and may face inflation, rising interest-rate, regulatory or geographical risk. Pension funds must carefully evaluate.

- Regional capacity: Even if capital is available, regional/local authorities and project sponsors must have capacity to develop, deliver and manage the investments. Without this, capital could be stranded.

What to watch / next steps

- Deal pipeline & announcements: Keep an eye on the number and size of projects announced under Sterling 20: housing schemes, broadband roll-out, regional regeneration, AI/fintech growth funds.

- Progress versus targets: The earlier Mansion House Accord set target allocations (e.g., 10% to private markets, 5% to UK assets). Sterling 20 will need to show how much capital gets deployed, timeframes, actual investments.

- Governance and transparency: How the partnership is governed, how projects are selected, how performance is measured, how risk is managed. The role of government vs market, how regional/local entities participate.

- Fiduciary oversight / regulation: Whether regulators step in to ensure pension trustees are fulfilling duties while participating in national-growth schemes.

- Returns and outcomes: For pension savers, whether these investments produce competitive returns, acceptable liquidity, and alignment with broader investment strategies. For regions, whether job creation, housing delivery, infrastructure targets are met.

- Market conditions / macro risk: Interest rates, economic growth, inflation, property markets; all can affect private market/infrastructure performance.

- Replication and scaling: Whether Sterling 20 becomes the start of a broader transformation (e.g., multi-fund vehicles, mega-funds, pooling of schemes) or remains a voluntary signalling initiative.

Summary

In short, Sterling 20 is a major move by the UK government and pension sector to mobilise large pools of long-term capital into the UK’s economy — especially infrastructure, housing, growth sectors, regional regeneration. It seeks to bridge the gap between pension savings and domestic productive investment, leveraging pension funds as engines of growth rather than just passive financial investors.

However, execution will be the key: capital mobilisation is one thing; delivering high quality investable projects, managing risks, aligning with pension savers’ interests, and showing tangible outcomes are another. If successful, Sterling 20 could mark a shift in how the UK leverages domestic savings for national growth. If it stalls, it may become another example of ambitious policy pledges meeting practical constraints.

Here are a few case-studies and commentary on the UK’s recently-announced Sterling 20 investment initiative (involving pension funds) — showing how it’s shaping up, what concrete commitments have been made, what the risks and commentary are.

Case-studies

1. Legal & General (L&G)

- L&G has announced a £2 billion commitment to “impact investment” by 2030 aimed at regional growth and regeneration across the UK. (Legal & General Group)

- The programme is targeted at housing, infrastructure and urban-regeneration; the press release says it will support ~10,000 new social & affordable homes and ~24,000 jobs. (Legal & General Group)

- L&G is explicitly cited as joining Sterling 20: “Investment programme will enable local and combined authorities to unlock their ambitions … the funding is from its balance sheet and co-investment from funds it manages on behalf of pension scheme clients”. (IFA Magazine)

- Why it matters: This is a large, tangible commitment by one of the major pension/insurance investors that gives substance to the Sterling 20 ambition of pension capital being channelled into “productive assets” in the UK.

2. Nest Corporation (NEST)

- NEST (the large UK workplace pension scheme) is reported as making commitments under the umbrella of Sterling 20: e.g., one article mentions “Nest will also provide Schroders Capital with £500 million – of which £100 million is expected to be channelled into UK investments … In addition Nest will invest £40 million, helping to deliver reliable broadband to rural homes and businesses.” (Shropshire Star)

- Why it matters: This demonstrates the initiative is not just about large insurers but also major pension schemes. Importantly the focus is on UK-specific themes (broadband in rural areas, UK private markets) rather than purely global assets.

3. Regional & Thematic Focus: Affordable Housing / Rural Broadband / Scale-up Finance

- The government’s description of Sterling 20 emphasises three key investment areas:

- Affordable/social housing (e.g., L&G’s 10,000 homes target) (Legal & General Group)

- Rural broadband/connectivity in less-served regions (e.g., NEST’s £40m for broadband) (Shropshire Star)

- Scale-up finance for high growth / private markets (AI/fintech etc) — the press release says the initiative will help “scale-up finance for growing businesses”. (Express & Star)

- Why it matters: These thematic examples show how the initiative isn’t generic but is trying to align pension capital with regional growth and national priorities (housing, infrastructure, connectivity, growth sectors). If delivered, it bridges pension savings & economic development.

Commentary & Observations

Positive commentary

- The Association of British Insurers (ABI) responded:

“Our pension sector is a powerhouse for driving growth. Collaboration is key … and the Sterling 20 is a bold step … Savers’ interests must always be at the heart of investment decisions, but with a co-ordinated approach we can work together to support a stronger economy today and savers’ futures tomorrow.” (ABI)

This acknowledges both the growth ambition and the need to keep pension savers’ interests in view. - The initiative follows on from previous commitments (e.g., the Mansion House Accord) which had targeted pension funds investing a higher share of assets into UK private markets. (GOV.UK)

- The push for pension funds to act collaboratively was also supported by the City of London Corporation / Lord Mayor of London:

“Too many foreign investors are put off by the lack of domestic lead investors … this initiative (Sterling 20) would build on that.” (MarketScreener UK)

Critical commentary / risks

- Some observers caution that the pipeline of investable projects is the key constraint. In previous years, UK pension funds invested far less in domestic assets (for example: only ~4.4% of UK pension assets in domestic equities in 2024) which shows structural under-investment. (theactuary.com)

- The Financial Times noted concerns: that unless there are “shovel-ready” and scaled projects, the initiative could remain symbolic. (Financial Times)

- Also, the balance between regional/national growth stimulus and fiduciary duty to pension savers remains a question: pension trustees must still act in the best interest of members, and if projects are riskier or less liquid this may expose them.

- One fund manager warned against further forced consolidation of pension-fund assets (into mega-funds) because oversized funds may lose agility and local responsiveness — a risk if the drive to invest domestically becomes too top-down. (Financial Times)

Summary Table

| Case | Key commitment | Theme | Comment / Significance |

|---|---|---|---|

| L&G | £2 billion by 2030 to housing/infrastructure/regeneration | Affordable homes + jobs | Provides a large, tangible anchor investment under Sterling 20 |

| NEST | ~£100 m into UK investments via Schroders + broadband rural investment | Private markets + connectivity | Shows smaller schemes participating & UK-themed investment |

| Thematic focus | Housing, rural broadband, scale-ups | Regional growth + productive assets | Illustrates how the initiative is intended to channel long-term capital into UK real economy |

What to Watch

- Project pipeline and execution: How many projects are actually announced, with value, region, asset type, timelines.

- Returns and risk outcomes: For pension savers, do these investments deliver competitive returns, acceptable liquidity, manage risk?

- Transparency & reporting: Will Sterling 20 participants publish commitments, progress, regions, sectors, impact metrics (jobs/homes etc)?

- Participation breadth: Are all major pension schemes engaged, or only a subset? How deep is the engagement?

- Balance of domestic vs global investment: Will UK-themed allocations displace other global opportunities, and can trustees show this is in savers’ interests?

- Regulatory / fiduciary oversight: Will regulators (e.g., The Pensions Regulator) or policymakers impose pressure or mandates if voluntary commitments lag?

- Risk of symbolism over substance: As commentators warned, without real deal-flow, this could end up as PR rather than transformative.