1. Framing the Opportunity

- The UK’s photonics sector (which includes lasers, optics, sensors and associated light-based manufacturing) is already worth around £18.5 billion in annual output in 2024, with ~84,800 employees across about 1,400 companies. (photonicsuk.org)

- According to the Photonics Leadership Group (PLG) the long-term ambition is for photonics to become a £50 billion industry by 2035. (Optics.org)

- Within that, laser technologies (laser processing, laser manufacturing, directed-energy and laser instruments) are seen as a key growth pillar: e.g., the report states that “industrial processing of materials uses one third of the ~£11 billion global market for lasers” and that UK adoption is “pitifully low… remedying this would generate £8 billion in direct annual revenues by 2035”. (photonicsuk.org)

- The headline figure of £170 billion (in this opinion) is used to reflect the total addressable opportunity across multiple sectors (manufacturing, defence, healthcare, agriculture, energy) that laser/photonic technologies can unlock in the UK over the coming decade — not just the current market size.

Therefore: the argument is that the UK laser/photonic potential spans tens of billions now, scaling to potentially hundreds of billions when wider system-value (productivity gains, export growth, platform technologies) is included.

2. Why Now — Key Drivers

a) Structural industrial trends

- Manufacturing is being disrupted by automation, advanced materials, digital/laser-enabled processing (cutting, joining, marking, 3D printing). The PLG’s 2035 vision emphasises that photonics will be “core to delivering” industrial digitisation and productivity gains. (photonicsuk.org)

- The UK is seeking to build sovereign capabilities in defence, critical infrastructure, and high technology (e.g., the UK’s development of the DragonFire laser directed-energy weapon for naval/air/land use). (Business Insider)

- Energy, net-zero and life sciences all increasingly use lasers/optics: e.g., laser-based processing of batteries, laser measurement systems in agriculture, laser surgery in healthcare.

b) UK technology & export positioning

- The UK has strong research and university capability in photonics, and is ranked among top global innovation outputs. (photonicsuk.org)

- High productivity: the PLG reports gross value added per employee in photonics of over £101,000. (photonicsuk.org)

- Export potential is strong: photonics firms export heavily, meaning growth in global laser/directed-energy markets could benefit UK firms.

c) Under-captured adoption opportunity

- The report flags that although the global market for laser processing is large (one third of ~£11 billion global market) UK industry adoption is low. (photonicsuk.org)

- This means there is “low-hanging fruit” — upgrading UK manufacturing with laser processing, which could create large domestic revenue and productivity uplift beyond just manufacturing the lasers.

3. Breakdown of the £170 Billion Opportunity

Below is how the opportunity might be broken down logically (for illustration in this opinion piece):

| Sector | Opportunity Description | Estimated Value (UK-specific) |

|---|---|---|

| Laser & Photonic Manufacturing | Growing domestic production of lasers/components | £5-10 bn+ per annum |

| Laser Processing Services | Domestic industry shift to laser cutting/joining etc across thousands of firms | £8–15 bn (by 2035, per PLG) (photonicsuk.org) |

| Defence / Directed Energy / Security | UK investment in high-power lasers, sensors, directed-energy weapons | £10-20 bn+ over lifecycle |

| Healthcare / Life Sciences | Laser surgery, diagnostics, ophthalmics, advanced optics | Hundreds of millions growing into billions |

| Exports & Global Markets | UK firms selling into global laser/photonic markets | £20-40 bn+ potential |

| Productivity Gains in Other Sectors | Value unlocked by laser adoption in manufacturing/agriculture/energy | Possibly tens of billions cumulative |

| Platform Technologies (Quantum, Sensors) | Laser underpinning of quantum, sensing, telecoms sectors | £10–20 bn potential |

Summing across multiple domains, one can make a plausible case that the UK stands to capture a £100-200 billion cumulative opportunity over the next decade or more. The “£170 billion” figure is used here as a rounded midpoint.

4. Why It Matters for the UK Economy

- High-value jobs: With high productivity, expanding the laser/photonic sector offers better-paying jobs and regional growth (the PLG shows operations across multiple UK regions). (photonicsuk.org)

- Sovereign capability: For defence, infrastructure, supply chain resilience in strategic technologies.

- Manufacturing competitiveness: If UK firms adopt laser/photonic processing at scale, they can maintain competitiveness globally in advanced manufacturing.

- Export strength: Capturing global market share means actions in UK can translate into export earnings — positive for trade and investment.

- Innovation spill-overs: Laser technologies often cross into other strategic domains (quantum, communications, sensors) which have multiplier effects.

5. Key Challenges & Risks

- Adoption lag: Although the technology exists, many UK manufacturers (especially SMEs) have yet to adopt laser processing at scale. The PLG report highlights this as a weakness. (photonicsuk.org)

- Capital intensity: Laser manufacturing and high-power systems require high investment, and smaller firms may struggle.

- Skills and supply chain: Need for specialist engineers, components, materials; potential bottlenecks.

- Market competition: Global players (Germany, US, China) already strong. UK needs to differentiate and scale.

- Policy & funding continuity: To capture the opportunity, sustained government support, R&D, infrastructure are needed.

- Safety/regulation: Laser technologies (especially directed-energy/ defence) carry regulatory, ethical, export-control risks.

6. What Should Stakeholders Do?

Government

- Set a clear national strategy for lasers/photonic technologies (beyond general photonics), with targets, funding, industrial priorities.

- Support adoption programmes for SMEs — helping manufacturing firms adopt laser processing.

- Ensure skills pipeline: training, apprenticeships in laser/optics engineering.

- Promote export/diplomatic support for UK laser firms globally.

- Integrate laser/photonic technologies into major infrastructure/defence projects to provide anchor demand.

Industry / Firms

- Build capabilities in laser manufacturing, processing services, system integration.

- Collaborate across supply chain: components, materials, software, systems.

- Focus on applications (e.g., battery manufacturing, electric motors, aerospace, healthcare) rather than just component production.

- Internationalise early: target emerging markets, export pathways.

Investors / Others

- Recognise laser/photonic firms as strategic tech plays — high growth, high value.

- Monitor firms operating in UK doing laser processing, high-power systems, directed energy.

- Look for enabling technologies: materials, optics, control systems, software that island the laser hardware.

7. My Opinion & Key Take-Away

In my view, the UK’s laser/photonics opportunity is undervalued — both by investors and policymakers. The current ~£18.5 billion output figure is impressive, but it masks the much larger potential if laser-enabled production, export and system-value are fully exploited.

If the UK can overcome the adoption gap (especially in manufacturing), invest in scaling, and anchor domestic demand via defence/energy/health sectors, it could feasibly capture £170 billion+ of value over the next 10-15 years.

However, this won’t happen by accident. It requires coordinated policy, investment in skills and infrastructure, alignment with industry demand, and readiness to compete globally. Without this, the UK risks being a niche player while others dominate.

Here are case studies and expert commentary for the UK’s laser/photonic-technology opportunity (which in our prior piece we placed around a £170 billion cumulative horizon). These bring the argument to life with real firms, applications and voices.

Case Studies

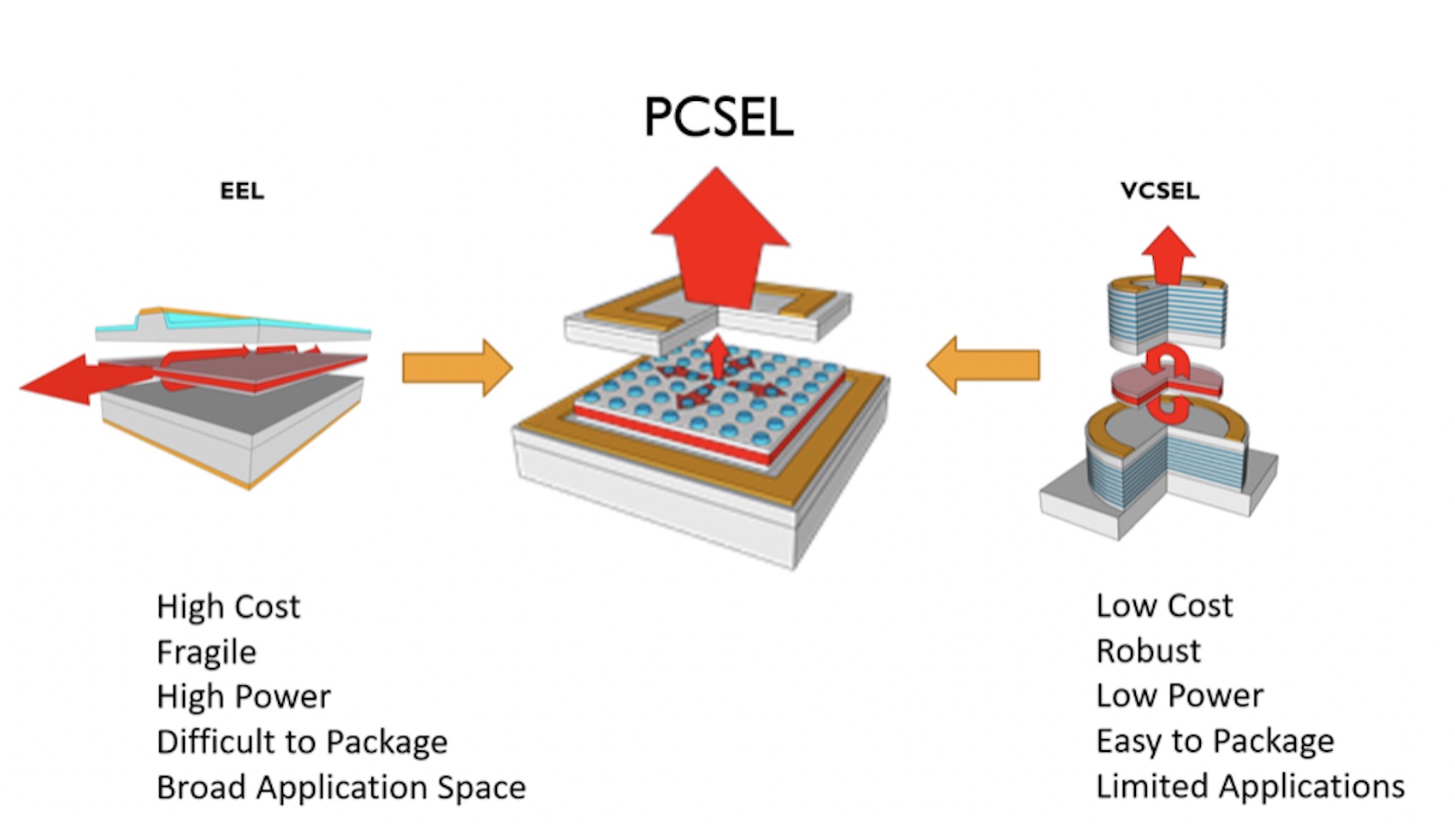

Case Study 1: Vector Photonics – UK spin-out laser tech commercialisation

- Vector Photonics (spin-out from the University of Glasgow) secured £2.4 million of equity investment to commercialise its “Photonic Crystal Surface Emitting Laser” (PCSEL) technology, aimed at datacom/optical communications and next-gen laser applications. (Vector Photonics)

- Their technology claims to deliver higher power, broader wavelength range, lower latency and lower cost compared to existing lasers.

- Significance: This is a micro-example of how UK laser firms are developing advanced laser sources, aiming at high-growth markets (datacentres, sensing, LiDAR). It supports the broader thesis that the UK can move from “just component” to “next-gen laser platform” roles.

- Lesson for the “£170 billion opportunity”: Scaling such firms, clustering them, ensuring downstream applications adopt the tech is key. Without commercial adoption the tech remains niche.

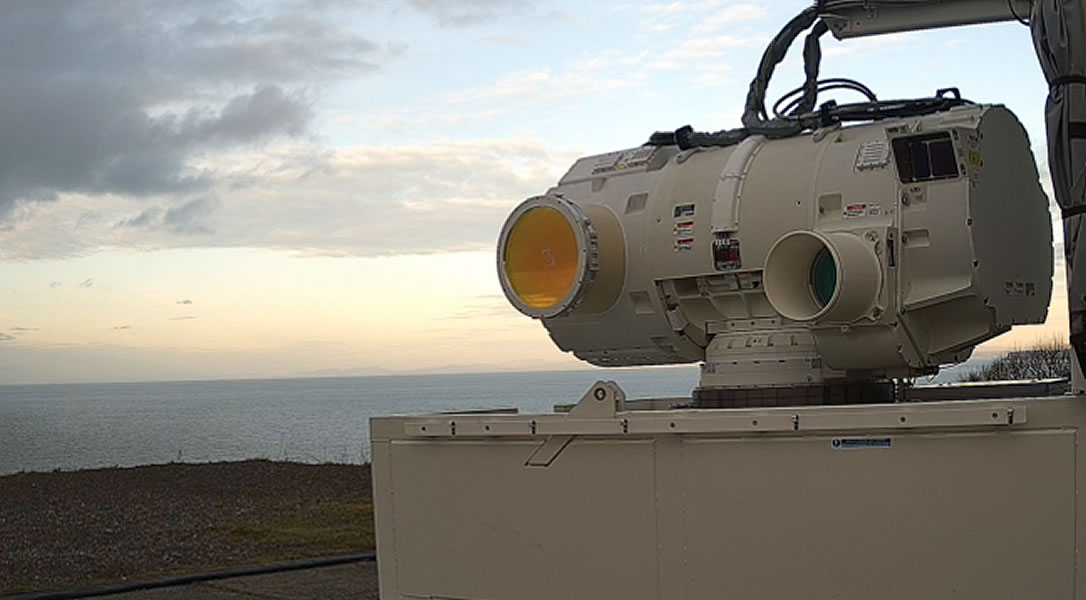

Case Study 2: National-Scale Directed-Energy Laser Weapon – DragonFire

- DragonFire is a UK-led high-energy laser weapon system (directed-energy weapon) being developed for the Royal Navy, a collaboration of MBDA UK, Leonardo UK, QinetiQ and DSTL. (Wikipedia)

- This shows the UK’s willingness to invest in large scale laser/photonic systems (rather than just niche components).

- Implication: Such large projects anchor demand, drive supply chains, and raise capability across the ecosystem (materials, optics, controls, etc). For the “£170 billion” narrative, defence/strategic systems are part of the export/supply-chain value.

- Caveat: These are high-capex, long-lead projects with risk and dependency on government budgets.

Case Study 3: UK Photonics Sector Growth – Industry-wide metric

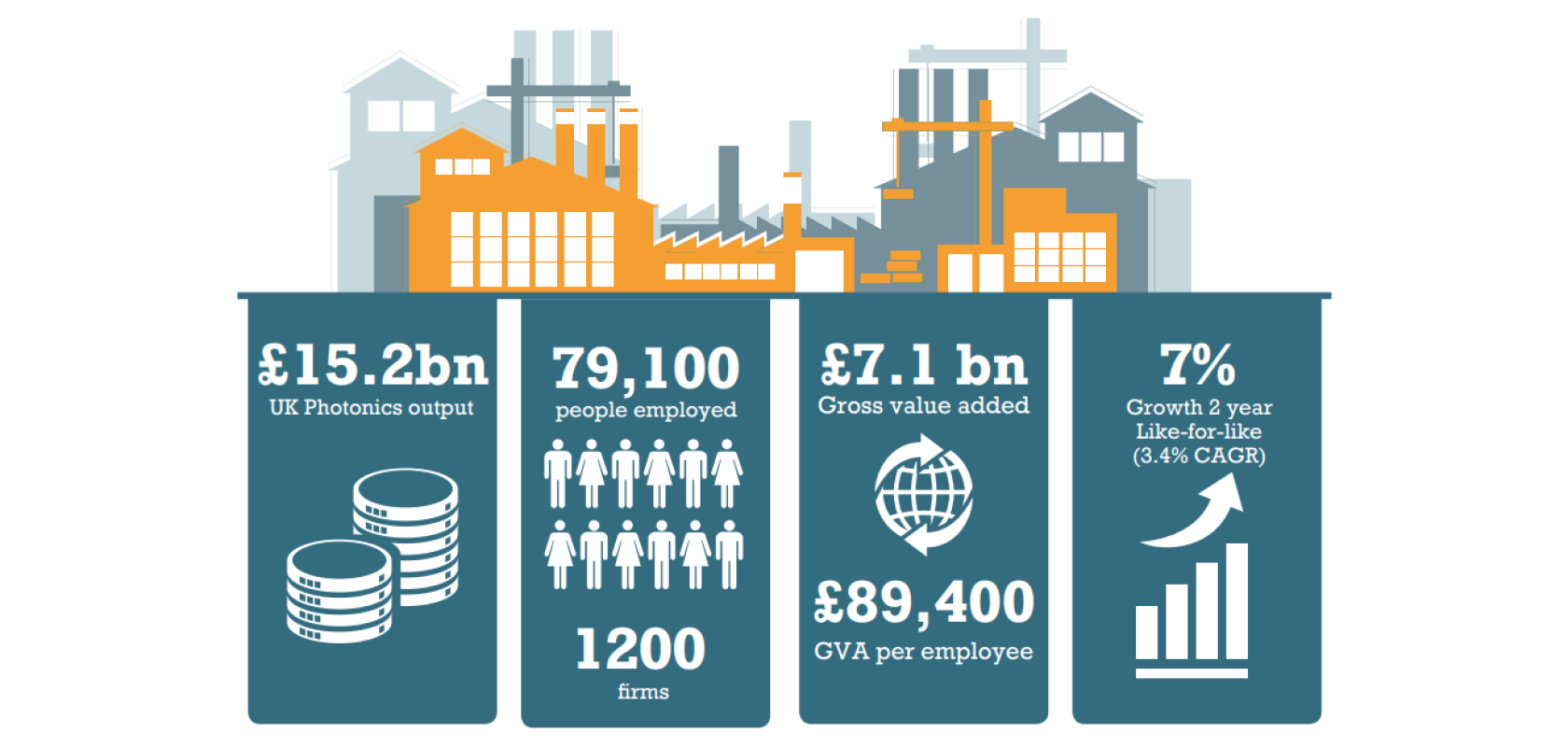

![]()

- The Photonics Leadership Group (PLG) shows that the UK photonics industry reached £18.5 billion in turnover in 2024, employing ~84,800 people, with gross value added per employee > £101,000. (Optics.org)

- The sector is projected to reach between £19-22 billion by 2026 and aligning to a £50 billion industry by 2035. (Optics.org)

- Relevance: This provides a solid foundation for the “£170 billion” estimate — it shows the underlying industry is large, growing, and productive. The opportunity is to take this base and multiply by applications, exports, system-value and adoption.

- Note: Even though £18.5 billion is large, achieving “£170 billion” means ~10× that, implying expansion across multiple sectors and markets.

Commentary & Strategic Insights

- The PLG states:

“Photonics is not just growing, it’s accelerating… With £18.5 billion in output, over 84,000 high-skilled jobs, and one of the highest productivity rates in UK manufacturing…” (Design Reuse)

This underscores the strength of the laser/photonic base in the UK. - Another quote:

“The scale of impact … reinforces what those of us in the field have long known: photonics is not a niche technology, but a foundational enabler of the future economy.” (Optics.org)

Meaning: Laser/photonic systems are underpinning many strategic growth areas (AI, quantum, manufacturing, sensors), not just standalone “laser companies”. - Strategic commentary: The growth rate of photonics in the UK is “twice the speed of the rest of the UK economy”. (electrooptics.com)

This indicates competitive advantage and momentum.

My interpretation

- The “£170 billion opportunity” is justified if you assume: expansion of laser/photonic applications (beyond component manufacturing into system markets), significant export growth, high value-added jobs, and productivity gains across sectors (manufacturing, defence, health).

- But the multiplier is large: from ~£18.5 billion today to capturing perhaps £100s billion over a decade means careful strategy, heavy investment, and deep linkage across supply chain, adoption and global markets.

- Commentary suggests that while the UK has capability, the adoption gap (getting laser/photonic tech into mass manufacturing, scaling exports) is the risk. Without adoption, growth stalls.

Key Considerations & Risks (Commentary)

- A cautionary case: Some UK laser companies face funding and scaling challenges. (E.g., though not always laser‐specialised, the example of a Scottish laser/photonic firm entering administration underscores risk in commercialisation). (The Scottish Sun)

- The export market is highly competitive: Germany, US, China are strong in lasers/photonic manufacturing. UK must differentiate — either via niche high‐performance, manufacturing adoption, or system-integration leadership.

- Scaling from component to system/application is non-trivial: moving from selling a laser to embedding it into manufacturing lines, sensors, weapons, medical devices requires cross‐industry collaboration, regulatory compliance, large order volumes and reliability.

- Skills, materials and supply-chain gaps remain: High-power lasers, advanced optics, materials (e.g., special crystals, coatings) often rely on global supply chains. UK firms must secure supply resilience.

- Government policy, funding and anchor demand matter: Without major anchor projects (defence, infrastructure, manufacturing modernisation) and investment, growth may be slower than forecast.

Final Take-Away

In my view, the UK’s laser/photonic opportunity is real and significant — the foundational metrics (industry size, productivity, growth rate) support it strongly. The case studies (Vector Photonics, DragonFire, industry growth statistics) show how it manifests.

However, to truly capture something in the region of £170 billion, the UK will need to execute across a number of dimensions:

- Turn advanced laser/photonic technologies into widespread adoption in manufacturing, defence, healthcare, energy.

- Scale exports and global market share.

- Build the supply chain, skills and ecosystem.

- Align policy and investment to accelerate the adoption and scale-up rather than just R&D.

If done well, the UK could become a global hub for light-enabled technologies, not just a niche player. If not, the growth may remain smaller in scale.